Changing times

Are you up to date with the most recent payroll legislation? Let Moore Stephens bring you up to speed

Recently there have been many changes to legislation regulating payroll. Business owners need to be aware of the following changes, which took effect from April.

CHILDCARE VOUCHERS

Having announced in the 2016 Budget that new applications for childcare vouchers would close on this April, the Government extended the entry deadline by an extra six months. This gives employees more time to decide whether vouchers or the Tax-Free Childcare (TFC) initiative – which helps with the cost of childcare – is better suited to them. The exact date is yet to be confirmed, but is expected to be in October 2018.

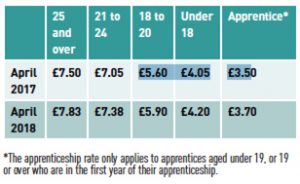

The Government increased the National Minimum Wage and National Living Wage rates, which took effect from 1 April. These changes see the largest increase in a decade to the 18-20 and 21-24-year-old rates. The new rates are:

PENSION CONTRIBUTIONS

The Government made a commitment to helping people save for retirement. As a result, the contributions you and your employees need to pay into workplace pensions are increasing. The phased rates, based on qualifying earnings, are as follows: There are also changes to the rates of Statutory Sick Pay and Statutory Maternity, Adoption, Paternity and Shared Parental Payments. Full details can be found at:

TAX ON TERMINATION PAYMENTS

Not all sums payable under a settlement agreement are tax free, so you need to break down the different elements of a package and consider each separately. From April 2018, the following are subject to tax and NICs:

• Payments in Lieu of Notice (PILON): Currently, if you don’t have a contractual right to make a PILON, any payment made in respect of an employee’s notice entitlement is generally regarded as ‘damages for breach of contract’ and the first £30k can be tax-free (and no NICs are due). Now, all PILONs will be taxable and subject to NICs, whether a contractual right is present or not.

• Post-employment notice income: If an employee doesn’t work their notice (for whatever reason) they still need to pay tax and NICs on any payments which correspond to the earnings they would have received if they had worked their notice. These earnings will be calculated on the basis of their actual earnings in the previous 12 weeks, including compensation for loss of taxable benefits (even if there was no PILON clause or it provided for basic salary only).

• Expected bonus income: This includes any bonus that the employee would’ve earned during their notice, or at another time, which relates to a time before their employment ended or the time that would have been their notice period. ‘Bonus’ includes commission, incentives or anything similar. • Tribunal awards for unfair dismissal, redundancy payments and contractual payments in lieu of redundancy will continue to benefit from the £30k exemption.

WHAT SHOULD YOU DO?

As an employer it’s your responsibility to ensure your employees are paid in accordance with the changes above. Automatic updates won’t be made to accommodate these changes, so sending the correct information to your payroll provider is important.

Need a hand?

Running a payroll efficiently requires sound processes. Moore Stephens provides a tailored service, offering simple advice or full support through a fully managed, outsourced payroll function. If you are uncertain how the above changes affect your payroll and the tax you as an employer will pay, or you’re considering outsourcing your payroll, contact us on 01536 461900 or visit www.moorestephens.co.uk

Image: www.freepik.com/free-vector/magnifying-glass-data-analysis_761448

Don't Miss!

-

Business

Moore UK’s New Podcast: unravelling your...

-

Business

5 reasons to digitalise your accounts in 2023

-

Business

Divorce | Who gets to keep the house?

-

Business

Meet your new business coach…

-

Business

Nene Park shines!

-

Business

Why you should use an accountant for Probate

-

Business

How are assets split in a divorce settlement?

-

Business

Parenting through separation | What happens if...